Response to AIER's Salter on Inflation and Interest Rates

Inflation expectations is a horrible economic variable and should be ignored.

Once again, a member of my community, brought this post by the AIER to my attention and said it was Ansel-relevant stuff. I responded to another one about a month ago. You can read it here.

In this post, titled, Faster Growth and Interest Rates: Even Harder than You Think, Salter lays out some opinions on the relationship between interest rates, Fed policy rates, and inflation. Salter is responding himself to Mickey Levy of the Wall Street Journal. Levy suggests that central banks have a problem with "inflation" because we have higher expected rates of return on capital. That will naturally keep inflation and interest rates higher than 2%. I tend to agree with that until it runs into recession. However, I'd like to respond to a couple points Salter makes.

First, Salter says the following:

The relationship between monetary policy and interest rates is complex. Rates indeed fall if the Fed unexpectedly loosens. But if looser money raises market participants’ inflation expectations, then nominal (current-dollar) interest rates will eventually rise. Hence, higher rates could be a sign of loose money, not tight, depending on how far from the policy change we’re looking and how fast the market adapts.

Let's take this piece by piece. The claim that the Fed "unexpectedly loosens" is wholly without foundation. When has that ever happened, at least in the last 30 or 40 years? I might be ignorant, but from my research, since Volker, the Fed has always started cutting rates AFTER market rates have come down.

The next sentence is like nails on a chalkboard. "Inflation expectations" should be banned for anyone who is honestly trying to understand the market. I know it is the cornerstone for modern central bank theory, but it is a catch-all term will little analytical value. It conflates prices and money supply, quality vs unproductive growth, and math with real life. It is the source of Salter's confusion in this post.

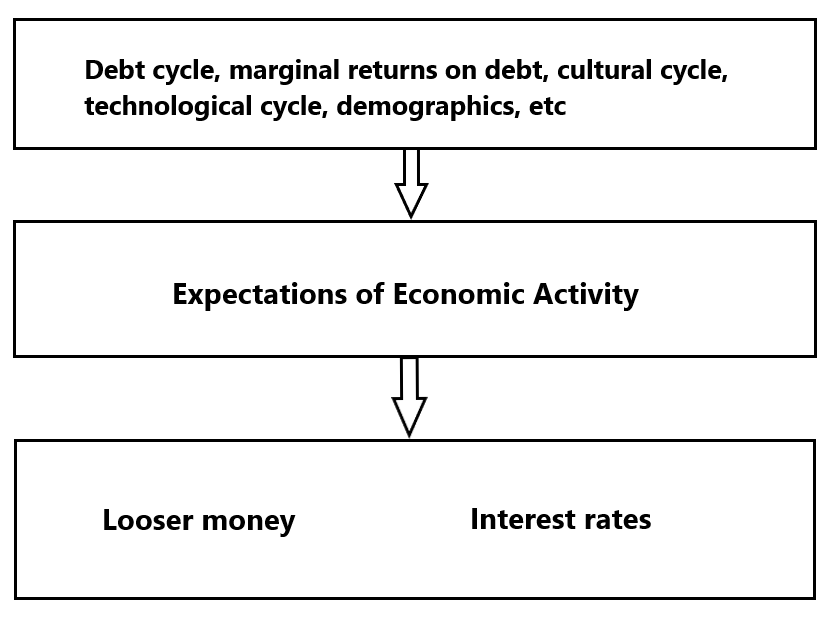

Inflation comes from net credit-expansion. Expecting higher inflation therefore is expecting higher net credit creation, a booming economy and growth. A more productive term would be "deficit expectations" for price concerns. Government spending is not technically money printing in an of itself, but it does temporarily increase circulating money supply, with an inflationary effect. Still more useful terms instead of "inflation expectations" would be "expectations of economic activity" or "experience of economic activity."

The sentence in question then becomes, "But if looser money raises market participants’ expectations of economic activity, then nominal (current-dollar) interest rates will eventually rise." Makes much more sense. It is still putting the cart before the horse. Looser money is itself the result of higher expectations of economic activity. We must separate that from cause and effect. Looser money and interest rates are in the category of economic effects, while expectations of economic activity (EEA) is a separate category.

One might argue that interest rates affect the debt cycle in a loop, but that is not the case. High interest rates don't matter if marginal returns on debt are even higher.

Salter continues:

Things get more complicated still when we consider the effects of economic growth. “Higher expected rates of return on capital have lifted real [inflation-adjusted] interest rates,” Levy argues. There’s a strong theoretical argument for this effect. Faster growth means higher lifetime income. Consumers would want to borrow against that larger future income to transfer some of that consumption from tomorrow to today, and businesses would want to do the same for investment purposes. The demand for capital rises, and real interest rates rise, too.

Now, this is good stuff. I'll add that higher returns on capital also carry higher risk and in our current state of affairs, higher fragility. He continues:

Real rates usually reflect structural economic factors; the effects of monetary policy are short-lived. We know from the Fisher equation that the nominal interest rate equals the real interest rate minus expected inflation. Mathematically, economists write this as i = r + E(π).

"We know". It is the prevailing academic wisdom, but it is not a law of nature. As I pointed about above, "expected inflation" is a red herring. What does expected inflation mean??? Is it price expectations, money supply growth expectations, what? How do you measure that? Would it be different with a different CPI methodology or formula? In a credit-based system, the important part of inflation expectations is expectations of economic activity.

Granted faster growth raises real rates (r), but by how much? We don’t know how sensitive real interest rates are to economic growth. There’s no reason to suppose, for example, that one-percentage-point-faster growth causes real rates to rise by one percentage point, and there’s certainly no reason to expect any measured effect to remain constant across the yield curve.

True, but we don't know exactly what affects inflation expectations, and how much, with your method either. What is growth?? Are all sources of GDP growth equal? If the government digs holes and fills them in, builds ghost cities and bridges to nowhere, produces 10 pharmaceuticals to treat side-effects of other pharmaceuticals, does that growth affect real interest rates all the same?

There are lots of unanswered questions because it is missing the point. An improper lens is being used. In 1960, in the Cold War, we could quantify "growth" as output. Today, the quality of the growth is at question. We might need to redesign the granddaddy economic metric of GDP itself.

In general, one percentage point faster growth lowers inflation by one percentage point. The nominal interest rate should fall one-for-one with economic growth, all else being equal. Now we have a case of ambiguous effects: the uncertain higher-real-rate effect against the one-for-one expected-inflation effect. Intuitively, real rates probably rise less than one-for-one when growth accelerates. But even if we know the direction of the effect, we still have a problem of magnitude.

None of these variables are in equilibrium. The desired measurements are, as noted, all else being equal. However, there are unknown unknowns in a market. I pointed out just a few in my diagram above, like cultural and technological cycles. Even demographics shift market behavior in unexpected ways. Salter correctly uses intuition here and identifies directionality as important. It is also rate of change, and the psychological effect of growth experienced today vs last year, or expected next year, etc.

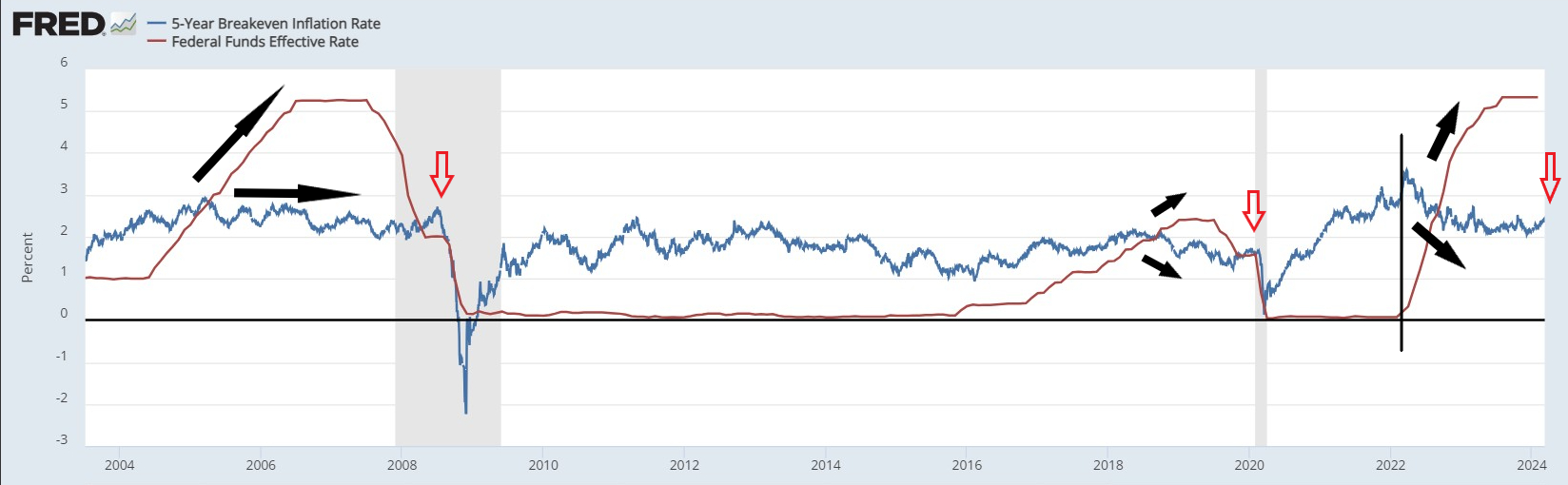

One more complication: the market’s expectations of inflation are rising, not falling, suggesting that the Fed might not have a grip on overall demand (total nominal spending) after all. Since February 1, the 5-year TIPS spread, which measures the breakeven inflation rate, has risen from 2.17 percent to 2.40 percent. The 10-year TIPS spread has risen from 2.19 percent to 2.32 percent.

Breakevens tend to have little spikes right before the crash (red arrows). They are not flat lines. We should expect small volatility and the current spike is not unusual. I also highlighted that Fed Funds does not correlate with breakevens. They rise and fall together sometimes, but many times they are completely opposite. 2014-2016 breakevens fell with rates at zero. Then 2016-2018, breakevens rose with rates. How does that work in Salter's theory?

To wrap up my brief response, I'll just point to the confusion felt by all these economists. The lens by which they view economics is not of a milieu and tapestry of a complex system, but of metrics, measures, dials and levers that central bankers can use to control the economy. I'm not saying there aren't things we can measure and relationship we can study, but if there is a belief in the central bank as the sun in the economic solar system, you are not going to make much headway.

As for interest rates and inflation going forward. There is overwhelming evidence of a looming recession. Recessions are deflationary, because it affects net credit creation. Low or negative net credit creation leads to lower interest rates.