History of World Reserve Currencies: Part 3 - Why European Currencies

A good question was asked by a reader that deserves to be addressed before we continue on to the Spanish real. They ask, "Does this series include only European currency?" The short answer is yes, but for good reasons.

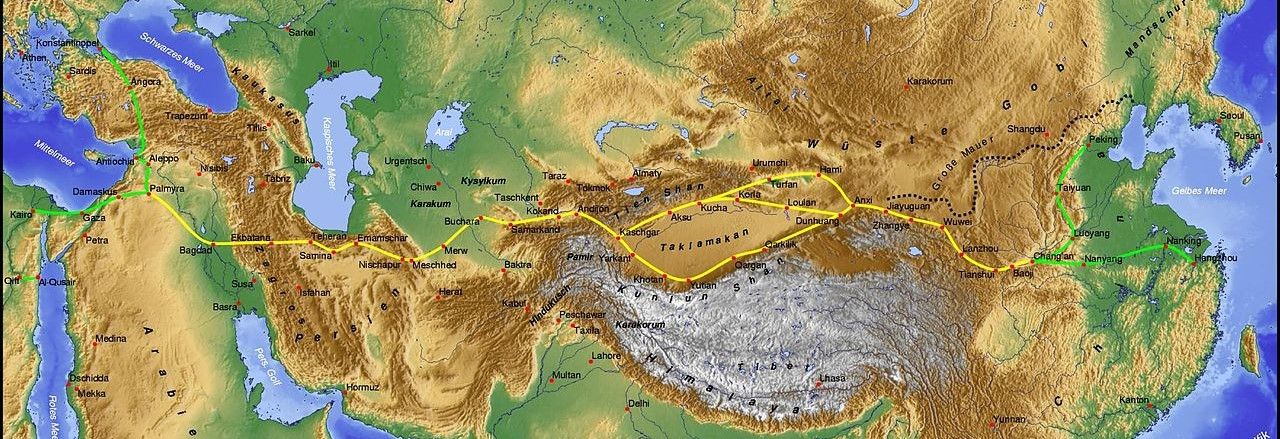

The Silk Road

First, our goal is to identify "global" reserve currencies and how they transition from one to the other. This mandates a standard currency commonly used throughout long-distance trade routes, bridging at least Europe and Asia. Until the modern era, international trade only made up a marginal amount of a kingdom's economic activity, most trade took place in local or regional trade networks, and the spread of specie was actively discouraged.

The Silk Road was a long overland trade route between East and West, with several periods of increasing and decreasing trade activity throughout the centuries. Total volume of trade, however, never reached critical mass or formed around a single currency. In some areas along the road, barter for horses, silk, or other luxury items took the place of money. In yet other places copper or bronze coins were used. No single currency for trade emerged along the length of the road.

The Silk Road's rugged mountains, harsh desert plateaus, and no east-west navigable rivers made travel slow. The lack of good paved roads made impossible the use of carts to carry goods, instead relying on low capacity camel caravans as the go-to mode of transportation. The road's many border crossings and frequent stops made it ideal for taxation and banditry cutting into the ability to make a profit. Only in periods of relative peace along most of the route did trade flow smoothly East to West (albeit slow).

Trade along the Silk Road was more like a diffusion of goods, rather than the nonstop trade route we imagine today. Traders did not travel the entire length of the road. Instead, goods diffused through a network of traders. For instance, merchants from Egypt might trade with merchants from Baghdad, who in turn might trade with merchants from Tehran or Samarkand, and so on. Local traders knew the land, language, and customs, so were able to make their way faster and more safely. Payments were also made along the way, whenever goods changed hands. Each subsequent trader took a small profit as they sold the goods locally and transported the remainder a little further down the road. This had the effect of not spreading currency like we imagine of more direct routes.

Mediterranean

The second reason for concentrating on European currencies is we start our tour at a specific time, the year 1250, the beginning of the modern trade currency. The two centuries between 1250 and 1450 witnessed many events that gave rise to large scale direct trade routes, displacing the slow diffusion along the Silk Road. Geopolitical and technological advances helped multiply trade volume and incentivize monetary convergence.

The Mediterranean, Black Sea, and navigable rivers in Europe, the Near East, and the Egypt, made this part of the world home to the most developed trade network. These merchants reaped high rates of return due to a superior mode of travel on water. Indeed, the merchant seafaring culture of the Mediterranean was able to quickly adapt to the changing geopolitical circumstances. Sea lanes remained open despite the shake up of Empires on land. These shake ups provided stimulus to even improve trade routes and methods. All this in turn created demand for a more consistent currency. As a comparison, sailing from one end of the Mediterranean to the other in Roman times, a trip of 4,000 km, would take roughly 4 weeks, while a 4,000 km trip along the Silk Road would take up to a year.

The convergence onto a single monetary standard is a property of larger more efficient trade networks. Where trade volumes reach critical mass, the natural forces of business will select a common currency. It is a synergistic relationship between trade volume and standardization of currency. We only saw this in pockets along the Silk Road prior to 1250, and to a much greater extent in the Mediterranean.

Snapshots of coins at points in history

As you can see below, the Greek drachma became the basis and etymological root for coins as well as their general denomination, prior to the era we are concerned with in this series. There is a common thread relating all the Western currencies back to Greece. The drachma was spread east by Alexander the Great, all the way to Bactria and India giving rise to the drahm, dirham, and dramma. The Roman denarius also began life as a drachma equivalent minted by Greeks in Italy. The weight of the denarius later became the basis of the weight in gold for the solidus, later copied by the Umayyads with the dinar.

In China, bronze and copper cash coins were most prevalent throughout history, and notably were replaced by paper money in circulation in the second millennium AD (denominated in copper cash). Gold and silver were rarely used in China except for some large transactions, using highly variable silver ingots called sycee. Of course, this was until they were exposed to high quality silver coins direct from European maritime trade.

Coins in 200 BC

- Silver drachma (minted from Sicily to India, but varied widely) (Athenian issue 4.3 g)

- Phoenician shekel (electrum, silver, bronze)

- Roman silver denarius (4.5 g)

- Chinese bronze Ban Liang

Coins in 100 AD

- Silver drachma (minted from Sicily to India) (~4.3 g)

- Roman gold aureus (8.1 g)

- Kushan gold stater (7.9 g) and copper drachma (2-3 g)

- China bronze Wu Zhu

Coins in 800 AD

- Byzantine solidus (4.5 g)

- Gold dinar (matched weight of worn solidus) (4.25 g)

- Silver drachm/dirham (minted from Spain to India)

- Chinese copper tongbao

- Carolingian silver denier

Coins in 1250 AD

- Silver drachm/dirham (minted from Spain to India)

- Gold florin/ducat (3.5 g)

- European denier

- Chinese copper cash coins and paper money denominated in cash (regional internal differences in alloys and weights)

{kind=link}